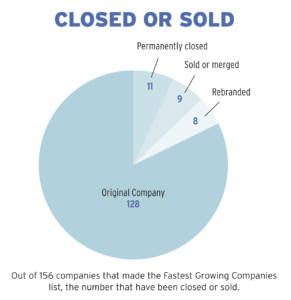

Each year, the Corridor Business Journal publishes its list of the fastest growing companies in the region, giving readers an insight into advancements local businesses are making in their respective fields.

But what happens to the companies that make the list through exponential growth, only to disappear a few years later? Why did those companies fold or become acquired? And what lessons can be learned from them?

A CBJ investigation into North Liberty-based Moxie Solar, a national solar installation business that was once named a Fastest Growing Company, examined strategic decisions made by leadership and the broken promises it gave to customers in the name of achieving unlimited growth.

The five-part series also looked at former CEO Jason Hall’s motivations behind starting the company, his attempts to keep the company afloat and future aspirations.

There’s no shortage of reasons that businesses can ‘rise and fall.’ What factors are outside of a leader’s control? How do decision makers deal with the pressures and expectations of the job?

The CBJ interviewed two former CEOs for such Corridor businesses, Eric Bochner of Bochner Chocolates and Greg Keeley of Asoyia, for the story.

Victim of circumstance

Mr. Bochner founded Iowa City-based Bochner Chocolates in 2003, hoping to capitalize on the luxury chocolate trend sweeping the country.

“There was a trend of people being more interested in high-end food products,” said Mr. Bochner. “Individual customers and also big retailers were very interested in offering new and different chocolate products.”

By 2009, the company was named the Fastest Growing Company in the Corridor, achieving 427% growth from 2006-2008. Sales peaked at $8 million a year, largely due to products shipped to big chains outside of Iowa and its retail store in Coralville.

A novelty project through a licensing deal with Hasbro allowed the company to create chocolate versions of Monopoly in a deal that shipped to Target and other retailers.

Demand was through the roof, but the nature of the business necessitated planning for several years out.

“When you’re doing manufacturing, there’s a long lead time,” he said. “You have to plan capital expansion maybe two years in advance. Then you have to order ingredients and do research and development maybe a year in advance.”

The demand that Bochner Chocolates became accustomed to ground to a halt once buying habits changed following the 2008 financial collapse. Discretionary income that customers might have spent on specialty chocolates vanished.

Since Bochner Chocolates wasn’t the only company that needed to get rid of now-unneeded equipment, the value of equipment also plummeted.

“It was a train that was already moving,” he said, “so it was a real shock to the overall system.”

Mr. Bochner said other business leaders agreed with his assessment: The 2008 financial crisis was a primary reason for the company’s struggles, as the business had just invested in products and infrastructure and was facing a maximum level of exposure.

“If we had just a couple more years of good execution [before the financial collapse], then I think our cash position and market position would have been more mature and cemented,” he said. “We would have had a much better chance of enduring that sort of problem.”

Three years later, the company was sold to Bissinger’s Handcrafted Chocolatiers of St. Louis. Mr. Bochner stayed on with Bissinger’s for six months before deciding to part ways.

“Like many acquisition deals, there’s a lot of potential,” he explained. “But the problem is that if you’re the entrepreneur that has built your business, it’s really hard to become part of another team. You have your own vision of how things are supposed to be done.

“I got into the business because I thought there was an interesting opportunity to deliver really nice, interesting chocolates to a market where there weren’t that many,” he added. “In the end, I just kind of decided that maybe it was just too hard of a project to get done.”

Cash flow a common theme

The CBJ’s Fastest Growing Company one year earlier was Asoyia, a maker of zero trans fat soybean oils.

Similar to Bochner Chocolates recognizing the trend of high-end foods, Asoyia saw a country ready to abandon the negative health side effects of trans fats, instead creating its own genetically modified soybean oil alternative.

At its peak during 2008, Asoyia experienced 851% growth and previously received $4 million from new investors, earning national media recognition from publications such as the Wall Street Journal. The company closed its doors just two years later.

“The real issue that we ran into was working capital, and, in essence, the cash flow situation,” said CEO Greg Keeley. “If you’ve got a whole year of supply chain, you’ve got to decide what you’re going to grow it, refine it, package it, store it and then eventually send it to a customer. You’re looking at several million dollars in capital that is tied up while you are waiting to sell this product to customers. It became very expensive for us to manage that supply chain.”

It’s a problem many fast-growing companies seem to face. While demand is often strong for a product that fits a market need, a company’s cash flow situation can create problems that spiral out of control.

Former Moxie Solar employees said the company faced similar cash flow and supply chain issues when Moxie began taking on too many projects in states outside of Iowa.

“We were projected to grow and triple our business every year for the next five years, which is a phenomenal growth rate,” said Mr. Keeley.”However, we were growing so fast that even the several million dollars that [investors] gave us turned out to be inadequate, relative to what we really needed to grow our business.”

Asoyia’s leadership team couldn’t find a buyer or investors for the company. Mr. Keeley hoped Asoyia would find a buyer five to seven years down the line, because the company was still growing so fast.

Instead, he resigned from his position with Asoyia in May 2010, warning the remaining team members that if Asoyia didn’t change how it was operating, the company would go out of business five months later.

“Sure enough, in about October of that year they announced they were going into bankruptcy,” he said.

Mental health impact

Leading a business throughout all stages of a company’s life cycle is a uniquely entrepreneurial enterprise that left a lasting impact on both Mr. Bochner and Mr. Keeley, although not entirely positive.

“The hard part is that you always felt every day you come to work, it was a level of dread,” said Mr. Bochner. “You knew something horrible was going to happen, you just couldn’t figure out what it was going to be that day. It always felt very existential in its threat.

“The hard part is that you always felt every day you come to work, it was a level of dread,” said Mr. Bochner. “You knew something horrible was going to happen, you just couldn’t figure out what it was going to be that day. It always felt very existential in its threat.

“When you start (the business), you think it’s going to be fun and interesting and exciting,” he continued. “But you don’t think ‘if we don’t get this done, what’s the impact of it?’”

He attributed some of that stress to working in a “high-leverage” environment with a lot of perishable inventory, a threat a software business, for example — a field he has a lot of experience working in — doesn’t face.

Mr. Keeley said that although he routinely put in 12-14 hour days, he “loved what he was doing.”

“In my opinion, it was the most fun job I ever had,” he said. “You end up learning all aspects of business. Not just the major aspects like cash flow and trying to find investors, but going out and finding an office location, buying chairs and furniture, washing windows by ourselves.

“It was stressful from the perspective that a lot of the investors in our company were the 25 original farmers that invested in the company,” he added. “And it was difficult to make them understand the whole cash flow situation that we were in, and how difficult it was to manage a small amount of working capital and to stay afloat at the same time.”

Lessons learned

Leaving these companies gave the CEOs space to reassess their business decisions. Could their companies have been saved?

Mr. Bochner said he would have done three things in hindsight: spend more time building the brand, engage with leaders in the industry and put together a board of directors, and to put a greater emphasis on his personal life.

“If I look back in retrospect, it was a great business adventure, but I think it had a lot of personal cost,” he said. “I won’t say that I have regret but … I probably didn’t evaluate what was required from a personal investment point of view.”

But despite knowing what he knows now, he’s still “not sure” the outcome would’ve been any different.

For Mr. Keeley, he said he would tell any entrepreneur to go find experienced mentors or consultants to get an objective opinion about the state of your business.

“When you get written up by the Wall Street Journal and people are calling you from all over, you kind of get enamored with what’s going on,” he said. “You kind of push aside the fact you still have to make the business work.”

Written by Noah Tong