By Chris Honkomp / Guest Editorial

It’s time again to think about end-of-year tax-planning.

With today’s complex economic environment and the myriad of changes that are occurring in 2013, it’s better to start too early than too late. I have outlined many specific items that are important to be mindful of as we finish out the year.

The following were made permanent by the 2012 Taxpayer Relief Act

• Lower individual income tax rates of 10, 15, 25, 28, 33 and 35 percent.

• Higher income tax bracket of 39.6 percent for taxable income over threshold amounts.

• Personal exemption and itemized deduction phase-outs.

• Capital gain and dividend tax rate of 15 percent in all but 39.6 percent bracket (0 percent for taxpayers in the 10 percent and 15 percent tax brackets)

Tax planning more complicated

While there is now more certainty in 2013 tax planning, higher-income individuals have to work with their tax professional to carefully structure financial transactions in order to minimize or plan for their additional tax burden. As always, rules about deducting passive losses and alternative minimum tax considerations add to the complexity.

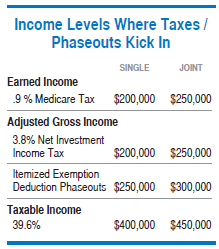

As noted above, there is the new 39.6 percent tax bracket, which becomes effective when taxable income exceeds $450,000 for married individuals filing joint returns and surviving spouses, $425,000 for heads of households, $400,000 for single individuals, and $225,000 for married individuals filing separate returns. In addition, a tax rate of 20 percent now applies to capital gains and dividends for individuals reaching into this bracket. There is also a reduction for allowed itemized deductions and personal exemptions if your adjusted gross income exceeds a specified threshold amount.

Medicare payroll tax

The employee portion of the Medicare payroll tax is currently 1.45 percent on all wages and self-employment income. But, at the start of 2013, this increased by 0.9 percent on wages and self-employment income over $250,000 for joint filers, $200,000 for individuals filers, and $125,000 for married couples filing separately. Employers are required to begin withholding the tax once an employee’s wages reach $200,000.

Medicare 3.8 percent surtax on net investment income

At the beginning of the year, a new 3.8 percent “Net Investment Income Tax” began applying to net investment income if modified adjusted gross income (MAGI) is over:

1. $200,000 single filer or head of household filer,

2. $250,000 joint return filer or qualifying widow, and

3. $125,000 married filing separately.

This tax will be based upon the lesser of the taxpayer’s net investment income or the excess of the taxpayer’s MAGI over the threshold amounts. Net investment income includes: income from interest, dividends, royalties, rents and annuities, and trade or business activities which are passive. While there is still a lot of uncertainty around this new tax, it’s important to work with your tax advisor to better understand how you may be affected.

So, the next time you ask “What tax bracket am I in?” and the answer is, “It depends……”, you will know why. The following chart may help you sort through the maze:

Since we have only touched the surface of the technical tax changes that have taken place this year, I recommend that you work with your tax advisor to proactively plan for your unique situation. This should help minimize your tax burden and, ultimately, achieve your personal and professional goals.

Chris Honkomp is a tax partner at Bergan Paulsen in Cedar Rapids.